eCommerce firms lose $31 billion annually on account of chargebacks. What began as a authorized mechanism to defend customers from fraud has turn out to be a persistent risk to the profitability of on-line retailers—in addition to a trouble for the customers who ought to profit from it.

Let’s take a look at how the chargeback course of works and why retailers ought to at all times maintain the variety of open chargeback requests to a minimal.

What are chargebacks?

Let’s begin with the chargeback definition:

A chargeback is a transaction wherein an issuing financial institution pulls funds from a service provider and provides them again to a shopper. This normally happens as a result of the buyer has escalated a dispute about a purchase order to their financial institution for decision.

A chargeback is totally different from a refund. As an alternative of contacting the service provider from which the acquisition was made and requesting a refund, a consumer can go on to their financial institution and request that the funds be faraway from the service provider’s account.

How are chargebacks used?

What’s a chargeback in easy phrases? It’s a mechanism designed to guard prospects from fraudulent retailers. At this time, nonetheless, we’re seeing the alternative drawback: fraudulent prospects profiting from trustworthy retailers.

Usually, a cybercriminal will acquire an individual’s card particulars and use them to make unlawful funds. The cardholder naturally has no thought till they occur to test their account or are contacted by the financial institution.

As soon as noticed, the cardholder can ask the issuing financial institution for a chargeback. The financial institution will examine the transaction in query and, if fraud is suspected, will forcibly take away the funds from the retailers’ account and return them to the cardholder’s account.

Chargebacks as a deterrent for retailers

Chargebacks are additionally meant to deter retailers from partaking in unethical or fraudulent practices. These would possibly embody delivering merchandise that don’t match the marketed specs or are faulty, accepting funds however not fulfilling the orders, or including hidden additional costs to the consumer’s card.

Since dissatisfied prospects have the likelihood to request their a refund by sidestepping the vendor altogether, eCommerce firms will usually attempt to present the most effective services to their purchasers. The overwhelming majority of companies are run this manner with none incentive. However for retailers who would possibly think about fraudulent exercise, chargebacks are a helpful guard.

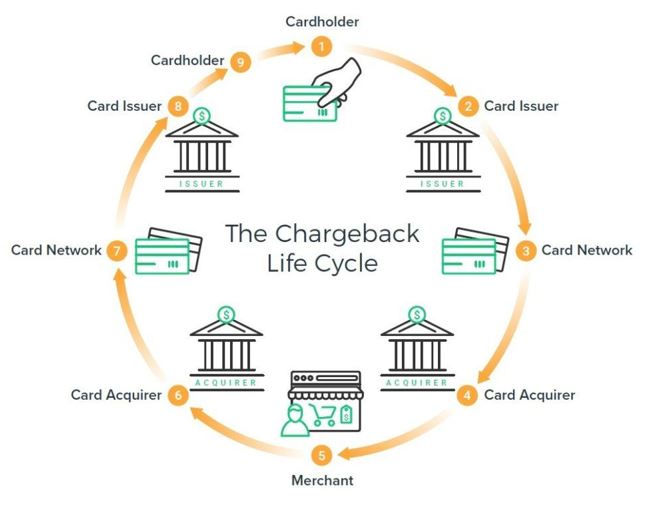

The chargeback course of

Right here’s a play-by-play of how chargebacks sometimes end up:

| 1. The cardholder disputes a transaction by contacting the card-issuing financial institution and requesting a refund.

2. The financial institution first checks if the transaction is eligible for a chargeback. In that case, the transaction is charged again to the service provider’s buying financial institution by way of the related card community: Visa, MasterCard and so forth. 3. The card community screens the chargeback for compliance in opposition to its technical standards. If confirmed, the chargeback is forwarded to the service provider’s buying financial institution. 4. The buying financial institution might switch the cash immediately from the service provider’s account to the cardholder, or ahead the request to the service provider first. 5. The service provider receives the chargeback notification and, if sure circumstances are met, can signify (i.e. oppose) the chargeback to its buying financial institution, offering documentation to indicate that the transaction was authentic and will stand. If the required standards aren’t met, the service provider should settle for the chargeback.

|

6. The buying financial institution forwards the service provider’s illustration to the cardboard community, who then forwards it to the cardboard issuer.

7. The card issuer then opinions the case once more and, if the service provider’s case is compelling, costs the cardholder’s account once more for the disputed transaction. Nevertheless, if the issuing financial institution considers that the chargeback subject has been inappropriately addressed by the service provider’s illustration, it could submit the dispute to the card community. This triggers arbitration by the cardboard community. 8. In arbitration, the cardboard community decides which occasion is chargeable for the disputed transaction. Ought to the service provider want to struggle the arbitration choice as effectively, there may be a further payment of roughly $500, though only a few transactions would justify the price of such an motion. |

What are probably the most frequent causes of chargeback requests?

In response to 48% of retailers, Card Not Current (CNP) fraud is the most important supply of all chargebacks, whereas a big quantity additionally comes from order not acknowledged complaints. Greater than 80% of customers admit that they’ve filed a chargeback out of comfort, which is slightly worrying.

Order Not Acknowledged

‘Order not acknowledged’ happens when the consumer doesn’t recall putting a brand new order or doesn’t acknowledge a transaction that’s listed on their financial institution assertion. It’s typically associated to subscriptions with recurring billing.

Most prospects don’t know (or bear in mind) that they agreed to be robotically billed for a services or products, actually because they only checked a field within the purchasing cart with out actually studying it, or as a result of the field was pre-checked they usually didn’t notice what it meant. Subsequently, they’ll dispute the cost.

Fraud

Fraud is more durable to detect and struggle, as it may possibly take many advanced kinds. Card Not Current (CNP) fee fraud has exploded lately in keeping with eCommerce, with cell funds and information breaches exposing customers’ information to fraudsters.

The 50% of fraud losses comes from ‘pleasant fraud’ and chargeback fraud.

- Pleasant fraud occurs when a member of the family buys one thing utilizing the consumer’s fee card with out them being conscious of it. Subsequently, when the cardboard holder sees the unknown order on their card assertion, they open a chargeback request.

- Chargeback fraud is when a consumer deliberately abuses their chargeback rights to each retain a bought merchandise and get their a refund.

The elevated shopper consciousness of chargeback rights and the convenience of disputing a cost—coupled with the issue retailers have in combating chargebacks—has led to an escalation in chargeback fraud lately.

Understandably, a rise in chargeback exercise has a substantial affect on a service provider’s backside line and is damaging for the eCommerce local weather total.

The intense affect of chargebacks

Bank card chargeback requests produce cascading results that ripple far past the refund prices themselves. For a begin, each single time customers file a chargeback request, the service provider is required to pay a chargeback payment—regardless of how the chargeback course of is finally resolved.

Chargeback charge

As well as, even when retailers dispute chargebacks and win these disputes, their chargeback charge doesn’t enhance.

| What’s the chargeback charge?

Chargeback charge is a metric that describes the ratio between the full variety of transactions and the full variety of chargebacks a service provider has earned. It’s calculated by dividing the variety of open chargebacks by the variety of finalized transactions within the earlier month. Why is that this necessary? As soon as chargeback charge creeps above a sure degree (roughly 0.9%) fee suppliers might terminate accounts with retailers. |

The typical eCommerce chargeback charge for retailers utilizing the 2Checkout digital commerce platform is between 0.3% and 0.4%. That is effectively under the 0.9 % threshold and thought of a really wholesome chargeback charge.

Danger of fines and penalties

Each chargeback request, legitimate or not, brings retailers one step nearer to fines and even shedding their service provider accounts with the buying banks.

Relying on the cardboard affiliation’s guidelines, fines imposed on retailers for exceeding chargeback charge thresholds can attain $10,000 or extra. Repeat offenses will then result in service provider account termination and probably inclusion on MasterCard’s MATCH record, which is able to forbid the enterprise from acquiring one other common service provider account with buying banks for 5 years.

Companies that discover themselves in such a scenario typically don’t have any recourse however to use for excessive danger service provider accounts, which normally include steep prices that lower deeper into the service provider’s profitability.

Chargebacks are a tough struggle for trustworthy retailers

The adverse affect of chargebacks is compounded by the truth that despite the fact that a reported 72% of retailers reply to chargebacks, the common internet win charge is just below 9%.

However, retailers can – and will – arrange preventative measures to defend themselves from chargebacks. Doing so won’t solely assist them keep away from vital revenue losses, but in addition contribute to the well being of world commerce total.

It’s 2023—What can I do to stop chargebacks?

All of it comes all the way down to offering an important buyer expertise: efficient and well timed communication in the direction of the consumer, transparency, responsiveness in customer support, and options and insurance policies that encourage buyer retention and discourage fraud.

Your greatest useful resource for actionable methods to scale back—and finally cease—chargebacks is our free e-book on Understanding Chargebacks. Test it out now and slash your chargeback charge!

{kind=link}