Within the dynamic panorama of the digital financial system, B2B funds play a pivotal position in shaping enterprise interactions. These transactions, occurring between companies quite than shoppers, facilitate the change of products, companies, and funds.

As we step into 2024, the importance of B2B funds intensifies, pushed by technological developments, altering shopper habits, and world market shifts. Fiscal yr 2023 witnessed an unprecedented surge in B2B funds, reflecting the rising reliance on seamless monetary processes.

From provide chain administration to cross-border commerce, B2B funds are the lifeblood of commerce, impacting effectivity, liquidity, and competitiveness. Let’s delve into the traits and challenges that outline this important area within the coming yr.

Pattern 1: Digital Pockets Adoption

Digital wallets have been witnessing an unstoppable development and adoption throughout the B2B cost panorama, reshaping the best way companies conduct transactions. The surge in cellular cost adoption, pushed by widespread smartphone utilization, has prompted conventional banks to adapt by providing tailor-made on-line banking options for companies.

The B2B digital cost market measurement is projected to develop considerably, from USD 4.2 billion in 2023 to USD 8.2 billion by 2028. This development is attributed to the regular improve within the adoption of strategies corresponding to e-wallets and digital playing cards.

Fintech sector’s development has launched progressive cost options, corresponding to digital wallets, additional driving the shift within the B2B funds panorama. Though digital adoption is comparatively new within the B2B funds, it’s a Fintech sector with a big market alternative.

The B2B cost panorama is quickly evolving, with digital wallets taking part in a pivotal position on this transformation. Companies are embracing this pattern, leveraging the comfort, pace, and safety provided by digital wallets to optimize their monetary operations.

Problem: Whereas digital pockets adoption is anticipated to surge within the B2B cost panorama of 2024, challenges corresponding to safety issues, interoperability points, and resistance to vary from conventional cost strategies can pose vital hurdles.

Pattern 2: Blockchain and Good Contracts

Blockchain’s basis is distributed ledger know-how (DLT), the place transactions are distributed and verified by a community of computer systems, guaranteeing transparency and safety. With its decentralized method, blockchain eliminates the necessity for intermediaries like banks, facilitating quicker and cheaper funds.

Cryptocurrencies, constructed on blockchain know-how, have gotten a beautiful choice for B2B funds. They provide benefits corresponding to quick cross-border transactions, decreased transaction charges, and elevated privateness.

Blockchain additionally facilitates programmable funds by way of good contracts, which automate cost processes based mostly on predefined situations. For example, JPMorgan is leveraging blockchain to make company transactions extra versatile and automatic.

Within the retail sector, blockchain and cryptocurrencies are making on-line funds safer and simpler, negating the necessity for patrons to pay extra costs.

Furthermore, blockchain is revolutionizing cross-border funds by offering environment friendly and safe options, overcoming the challenges of conventional banking techniques.

Cryptocurrency and blockchain know-how are reworking the B2B funds panorama by providing safe, clear, and environment friendly options. Their affect is anticipated to develop considerably within the coming years.

Problem: Regardless of the potential of blockchain and good contracts to revolutionize B2B funds, their adoption faces obstacles like regulatory uncertainty, lack of technical understanding, and scalability points.

Pattern 3: Actual-Time Funds

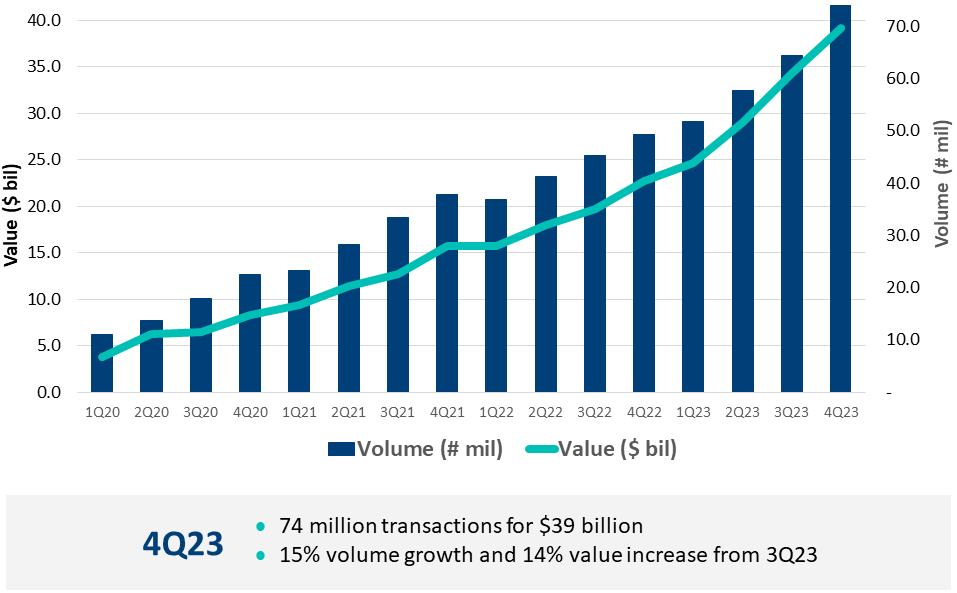

Actual-time funds (RTP) have develop into a big pattern within the monetary world. Because the identify suggests, RTP are funds which are processed immediately, constantly, and around the clock. With RTP, transactions between financial institution accounts are initiated, cleared, and settled inside seconds, whatever the time of day.

Actual-time transactions have been recognized as one of many key traits to form the way forward for B2B funds. RTP networks, such because the one supplied by The Clearing Home, allow shoppers and companies to conveniently ship funds instantly from their accounts.

Supply: The Clearing Home

The macro setting right now calls for effectivity positive factors, additional automation, and value reductions. Actual-time funds, providing quick funds availability, align with these calls for, enhancing operational effectivity, and bettering money circulation administration for companies.

Furthermore, the real-time steadiness characteristic of RTP provides a affirmation of funds. As soon as a cost is allowed, the payer’s account displays the deduction of funds instantly. This characteristic provides one other layer of safety and belief within the cost course of.

Importantly, RTP function on a 24/7/365 mannequin, permitting customers to ship and obtain funds at any time. This continuous operation is very helpful for world companies that cope with totally different time zones.

The rise of real-time funds is ready to remodel the best way companies deal with transactions in 2024, providing safe, environment friendly, and instantaneous options.

Problem: Actual-time funds promise instantaneous, 24/7 transactions for companies. Nevertheless, integration complexities, information safety points, and the necessity for world standardization can impede their widespread adoption.

Pattern 4: Embedded Finance and APIs

Embedded finance, powered by APIs, is anticipated to develop into a big pattern within the B2B cost panorama of 2024. This progressive method permits companies to combine monetary companies instantly into their current product choices.

In B2B , embedded finance can streamline the cost course of, scale back guide duties, and reduce potential errors. The combination of APIs permits seamless connection to third-party monetary companies, making these advantages accessible inside current enterprise platforms. For example, e-commerce websites providing loans, social media platforms introducing cost functionalities, and cost facilitators are all examples of how embedded finance is being leveraged.

The market measurement for embedded finance within the B2B sector is predicted to increase considerably. Anticipated to develop to $6.5 trillion by 2025 (from $2.5 trillion in 2021), the potential for B2B functions is huge.

Embedded finance and APIs are set to reshape the B2B funds panorama in 2024, providing extra environment friendly, built-in, and customer-friendly cost options.

Problem: Take into account that embedded finance and APIs are set to reshape the B2B funds panorama, however challenges like guaranteeing information privateness, managing third-party dangers, and dealing with regulatory compliance can come up.

Pattern 5: Cross-Border Cost Improvements

Cross-border funds have been revolutionizing the B2B panorama, witnessing constant development and paving the best way for a transformative 2024. This sector, at present the fastest-growing section within the cross-border area, is primed to reshape world commerce.

The expansion of cross-border funds within the B2B realm might be attributed to some key elements. Firstly, digitalization has performed a big position, offering companies with the instruments and platforms needed to simply facilitate worldwide transactions. Secondly, the growth of worldwide commerce has pushed demand for environment friendly, dependable cross-border cost options.

Regardless of making up lower than 20% of the overall market by 2030, B2B cross-border funds are a pressure that can not be ignored. The market witnessed a gradual improve of $14 trillion with a development charge of 10%, from $137 trillion. This determine is anticipated to rise 53% to $290.2tn in 2030.

In 2024, the cross-border funds section is anticipated to develop on the highest CAGR of 11.63% within the B2B funds market. This development is fueled by the rising significance of cross-border transactions in supporting the expansion of business-to-business commerce and commerce.

The surge in cross-border funds is ready to considerably impression B2B transactions within the following yr and past. As companies proceed to globalize, the demand for environment friendly, safe, and quick cross-border cost options will solely improve.

Problem: Improvements in cross-border funds are shaping B2B transactions, but they will face hurdles corresponding to excessive transaction prices, regulatory complexities, and points associated to international change volatility.

Conclusion

Because the market continues to develop and evolve, companies should adapt to new applied sciences, buyer preferences, and regulatory necessities. The traits we have now mentioned on this weblog publish present alternatives for corporations to innovate and improve the shopper expertise.

Staying forward on this dynamic setting requires an knowledgeable and proactive method. It’s essential to know not simply the alternatives these traits current, but additionally the potential hurdles that may come up. By doing so, companies can strategically navigate the altering panorama and harness the facility of those traits to drive development and effectivity.

{kind=link}