Regardless of decarbonization targets, emissions from heavy-duty transport have risen steadily for many years — tailpipe emissions are estimated to have risen over 2% per 12 months since 2000. After a slight drop through the pandemic, heavy-duty automobiles (HDV) emissions, significantly from freight transport, have continued to climb. HDVs at the moment are are chargeable for over 25% of highway transport emissions within the EU whereas making up solely 2% of the highway transport fleet.

Amongst HDVs, vehicles are a specific ache level for decarbonization and emissions reductions. Globally, heavy-duty vehicles account for over 40% of freight emissions and are chargeable for as much as 80% of the rise in tailpipe CO2 emissions over the previous twenty years. Decarbonizing heavy-duty transport is rising as a precedence goal for native and nationwide governments to fulfill transport decarbonization targets. Norway, the UK, EU, and California have all proposed or carried out bans on the sale of recent diesel HDVs between 2030 and 2040.

Limits to Battery Electrification

Whereas battery electrical automobiles (BEVs) appear to be the clear pathway in the direction of reaching net-zero passenger automobiles, electrification alone is not going to be ample to decarbonize heavy-duty transport. A number of key traits of industrial quality transport make BEV HDVs impractical:

- Charging time: Class 8 long-haul vehicles that require roughly 1-2MWh batteries can take as much as a number of hours to totally cost, rising journey instances by as much as 35%. For logistics and freight fleets already working on slender margins, this extra drive time shouldn’t be economically possible.

- Payload: The batteries required for heavy-duty industrial automobiles considerably scale back obtainable cargo capability — probably over 8,000 kilos. Lowered cargo capability and elevated car weight additionally negatively impression the operational economics, and considerably enhance the payback time on the upfront value of buying a BEV HDV.

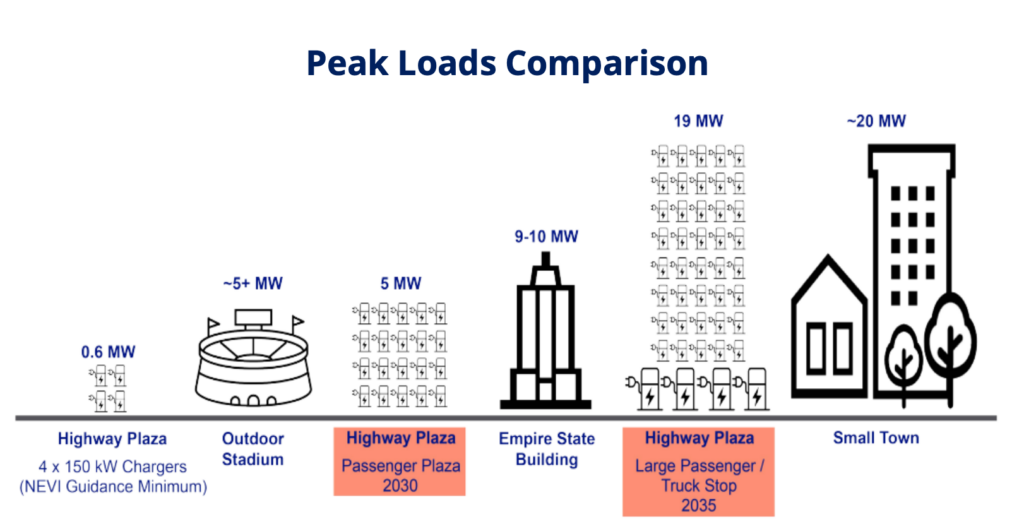

- Charging infrastructure: Bodily infrastructure deployment and electrical energy requirement:

- Charging stations for HDVs require considerably extra space than passenger automotive charging stations as a result of longer cost time of the bigger automobiles. Excessive use fee and shorter vary additionally will increase the variety of stations required throughout long-haul routes.

- Megawatt charging locations a large demand on {the electrical} grid. Widespread megawatt charging would require a mixture of onsite renewable power technology and power storage.

Hydrogen Use Case: Lengthy-haul and Again-to-base Transport

Utilizing hydrogen to gasoline HDVs (both with hydrogen combustion engines or hydrogen gasoline cells) addresses a number of of the challenges dealing with BEVs within the heavy-duty transport sector. Specifically, the cost time for heavy-duty hydrogen vehicles is 10-Quarter-hour, comparable to traditional diesel automobiles. Equally, payload is minimally affected, significantly for long-haul and heaviest-duty automobiles.

Whereas hydrogen gasoline cell automobiles (HFCEV) make the most of each battery packs and hydrogen gasoline cell techniques, the batteries are considerably smaller than absolutely BEVs. Hydrogen vehicles even have the aggressive benefit when it comes to vary compared to BEVs, with newer fashions reaching as much as 800 miles. Longer-range, shorter refuelling instances, and elevated cargo capability enhance the economics of hydrogen HDVs, shortening payback time and rising productiveness for fleet operators.

Challenges and Innovation

- Hydrogen vehicles are at the moment 2x-4x the value of diesel vehicles, which is prohibitive for many fleets.

- With hydrogen storage, high-volume, low-mass fuel have to be saved both at excessive strain or cryogenic temperatures:

- Storage tank weight and dimension impression payload and vary — pressurization and cryogenic temperatures increase security issues.

- Lack of established refueling infrastructure and restricted car availability stall buyer uptake — rooster or egg – not sufficient automobiles to justify infrastructure growth, lack of infrastructure stalls car uptake.

Innovators are addressing these challenges, partaking throughout the worth chain to supply hydrogen refueling options, storage, and gasoline cell system optimization, in addition to fast-tracking car availability and manufacturing.

- Retrofitsof diesel vehicles for hybrid gasoline compatibility or hydrogen gasoline cell powertrain eliminates upfront value of buying new fleet automobiles. The shorter manufacturing course of will get automobiles on the highway a lot sooner than bespoke car manufacturing (e.g., Hyzon Motors).

- Software program options optimize diesel displacement and hydrogen gasoline use (g., Hydra Power).

- Hydrogen storage: Cryo-compressed and sub-cooled hydrogen enhance power density and enable for elevated vary, payload, keep away from the excessive value of liquefaction, and scale back gasoline losses (e.g., Verne).

- Refueling: Innovation is clear in modular refueling providers, hydrogen-as-a-service, and vertically-integrated hydrogen producers (e.g., Pure Hydrogen).

- Inexperienced hydrogen producers are partaking in ecosystem-building, bespokeinfrastructure, car procurement, and refueling options (e.g., Phynix).

Wanting Ahead

Hydrogen availability and value are key uncertainty elements for fleet operators trying to purchase net-zero HDVs. Inexperienced hydrogen manufacturing and gasoline mandates, zero emissions car subsidies and incentives, and federal funding for fueling infrastructure will make hydrogen HDVs a extra enticing possibility.

In the meantime, retrofitting current diesel HDVs for hydrogen shall be essential to get hydrogen HDVs on the highway, carry out larger-scale pilots, and justify the deployment of widespread hydrogen refueling infrastructure. Preserve a watch out for exercise from main auto incumbents. The entire largest truck producers have introduced manufacturing or launched pilots of hydrogen HDVs in recent times. Anticipate automobiles from OEMs to hit the roads within the final 2020s.

{kind=link}