Up to date in October 2023.

Within the dynamic world of eCommerce, stagnation will not be an choice. As digital storefronts develop into the norm and client preferences shift at lightning pace, understanding and adopting the newest fee tendencies is paramount. It’s not nearly facilitating a transaction; it’s about enhancing your complete procuring expertise.

For companies seeking to develop, holding a finger on the heart beat of fee improvements is a necessity. Strap in as we discover the world fee tendencies set to form 2024 and past.

On-line Fee Tendencies

On-line funds have undergone an enormous transformation lately. Let’s unpack the foremost on-line fee tendencies which might be redefining the eCommerce panorama.

Contactless funds take heart stage

NFC (Close to Discipline Communication) has been embedded in some bank cards since 2007 within the UK, however right this moment greater than 80% of credit score and debit playing cards have built-in contactless.

After all contactless is considerably sooner and simpler than chip-and-pin, however the primary purpose for its reputation is the cell pockets. The likes of Apple Pay, Google Pay and Samsung Pay enable customers to make purchases with the one system that’s virtually at all times on their individual—their telephone.

With the power to carry a number of debit & bank cards, plus options like PayPal, cell wallets has revolutionized the fee expertise for customers.

Contactless as a response to Covid-19

As soon as Covid-19 was recognized to transmit by way of surfaces, the need for contactless as a protected fee technique skyrocketed. Many companies and retailers shortly tailored by upgrading their fee programs to just accept contactless funds, driving even wider adoption from customers. In Italy, contactless utilization went up by 83%, whereas in Germany, it rose by 42%.

Covid was a serious set off for elevated spending limits by way of contactless. Transactions have been initially restricted to small quantities, however a number of nations in Europe have now set €100 limits (or increased) on contactless spending. Within the United States, there isn’t a restrict in any respect.

This behavioral shift is anticipated to have lasting implications for the fee business, with contactless funds more likely to stay a dominant fee technique within the post-pandemic world.

Embrace different fee strategies

The exponential rise in comfort isn’t restricted to contactless funds. A revolution has additionally begun in embedded finance, an answer the place companies take funds straight inside their platform or app. For instance:

- Journey-sharing apps providing in-app wallets

- eCommerce platforms offering on the spot loans

- Social media platforms enabling peer-to-peer funds

Supporting a variety of other fee strategies is a vital differentiator within the digital age. The flexibility of non-financial corporations to supply monetary providers creates a extra seamless person expertise.

One other instance is the Purchase Now, Pay Later (BNPL) phenomenon. The place staggered funds was the hallmark of credit score establishments, now nearly any on-line vendor can provide installments or deferred funds.

Whereas interesting, BNPL does create threat for each events. For corporations, money is king and overreliance on deferred funds is rarely comfy. However for customers, the benefit of accruing debt, curiosity and late charges is staggering. The results on long-term monetary stability and credit score scores will be damaging. There’s a lot to think about earlier than providing, or accepting, a BNPL plan.

Enhanced safety and biometric authentication

The rise in contactless and embedded fee options is accompanied by elevated consideration to safety and laws, because the comfort of these strategies can be exploited; within the United States, the place there are no contactless fee limits, stolen smartphones or phished login particulars can lead to unauthorized purchases till reported.

Biometric authentication, similar to fingerprint readers in smartphones, gives increased safety and ease of use in comparison with conventional strategies like passwords or PINs, gaining reputation amongst customers, and paving the best way for gradual acceptance of facial recognition, regardless of some preliminary challenges.

Localization will probably be extra crucial than ever

The on-line fee panorama for worldwide sellers has develop into numerous. Every area has distinct preferences. Bank cards stay dominant in North and South America, however in Europe fee wallets (like PayPal) are extraordinarily fashionable. In response to the Baymard Institute, 6% of US buyers abandon their cart if their most popular fee technique is unavailable.

One thing all of us have in frequent is the need to pay in our native foreign money. It’s a aggressive drawback to refuse native fee strategies. However the fee ecosystem is dynamic. New fee strategies emerge and previous ones evolve. Staying up to date with these modifications is important for companies to stay related.

For manufacturers world enlargement, localized funds are a vital pillar for an excellent buyer expertise.

Bonus: Uncover these actionable ways to maximize your income by recovering deserted carts in your on-line retailer.

Cryptocurrency and digital property

Cryptocurrency might not have seized conventional banking, however it’s gaining traction as a viable fee choice, particularly Bitcoin and Ethereum. There’s a rising market of customers and distributors who champion the decentralized nature of cryptocurrency. Giants like Microsoft, Tesla and Entire Meals already settle for cryptocurrencies; eCommerce is more likely to comply with.

In concept, cryptocurrencies provide superior safety, decrease transaction charges and are completely borderless. Whereas these elements are massively interesting to world manufacturers, the challenges—like their rampant volatility and evolving regulation—make imminent adoption on a mass scale unlikely.

Offline Fee Tendencies

Offline and in-person funds are always evolving with expertise and client expectations. More and more, the road between on and offline is blurred. Let’s take a look at the important thing tendencies which might be shaping the way forward for offline funds.

Good POS programs and integration

The evolution of conventional POS programs into good, related gadgets has revolutionized the retail business. Past processing funds and printing receipts, good POS terminals have touchscreens, web connectivity and the power to run third-party apps. They’re safer and have a versatility that works with all the things from retail to hospitality.

Integrating offline and on-line knowledge is by far essentially the most highly effective good thing about good POS programs. Manufacturers can monitor the shopper journey throughout channels; they will make data-driven choices and optimize stock administration, advertising and gross sales.

Whereas POS programs are ostensibly offline merchandise, they’re being catapulted into the digital age and are giving brick-and-mortar companies the chance to scale their on-line exercise extra simply.

QR code funds

QR codes owe their large resurgence to the Covid-19 pandemic. One space QR codes dominated was hospitality: they turned the go-to technique of sharing each menus and fee choices for eating places and bars. Prospects scan the code, browse the cell web site, place their order and put their ft up.

QR codes are easy, manufacturers can create them totally free and get inventive with their implementation. However whereas most elements of each day life have returned to regular, QR codes have caught round. They continue to be significantly fashionable for person-to-person funds: merely scan the code to launch PayPal or Venmo, with all of the fee info immediately generated. Gone are the times of slowly inputting financial institution particulars for guide transfers.

Whereas QR codes want testing and will be finicky to arrange, they run effectively and make life extraordinarily simple for customers. Removed from a fleeting pattern, the QR codes are solely gaining popularity.

Actual-time funds

The world will by no means return to the days of gradual funds. Actual-time funds supercharge money move, enable manufacturers to immediately ship fee confirmations (which builds belief) and will be performed throughout the globe. It’s most likely the only largest innovation in fashionable banking.

As at all times, the true demand for real-time funds comes from customers. As they develop into extra accustomed to instantaneous providers in different areas of their lives, they anticipate the identical when making purchases.

The expansion of real-time funds will be attributed to technological developments and improvements within the fee sector. Fashionable infrastructure and programs have made it attainable to course of funds in real-time, and each customers and companies have grasped the chance with each fingers.

Like QR codes, the worth of real-time funds will not be restricted to any sector or business. They’re getting used for all the things from peer-to-peer transfers to main enterprise transactions. And when everybody will get paid sooner, it has a robust and constructive impact downstream. Developments will come thick and quick as extra funding is made within the expertise.

Voice-activated funds

Whereas voice-activated assistants are seen as gimmicks by many, they’ve develop into immensely fashionable. The likes of Amazon’s Alexa, Google Assistant, and Apple’s Siri combine with telephones, good properties, audio system and even vehicles. And now customers can provoke transfers, test account balances and even make purchases simply by talking to their system.

This hands-free strategy is being leveraged by all types of customers and is very helpful for visually impaired people or those that discover conventional fee strategies cumbersome. It additionally gives a brand new channel for gross sales & engagement for manufacturers.

However unsurprisingly, there are main safety issues.

Voice recognition is nowhere close to as strong as biometric sensors or the PIN code. Methods can simply misread instructions and voices will be mimicked. How precisely the business will overcome these vulnerabilities is unknown. Finish-to-end encryption, multi-factor authentication, and steady monitoring for suspicious actions will probably be essential.

Downstream from safety issues is the difficulty of adoption: most individuals don’t like experiments in the case of their cash. Customers want near-absolute assurance that their cash is protected and that the expertise is dependable. Till that’s supplied, voice-activated funds will proceed within the small minority of fee strategies.

Sustainable and inexperienced fee options

Whereas the funds business is taking strides in the direction of sustainability, it’s laborious to see their efforts as far more than token gestures. Fee playing cards from sustainable supplies are good, however supplied by a tiny variety of paid accounts.

Digital receipts are the opposite big-hitter in sustainable funds. Whereas the eradication of paper receipts is welcome (and lengthy overdue) adoption is restricted. The first good thing about digital receipts might be ease for the buyer, somewhat than environmental conscience.

Carbon offsetting is one other alternative for fee corporations to affect change. For instance, a portion of transaction charges will be directed in the direction of environmental tasks like planting timber, supporting renewable power tasks or different carbon offset applications. It is a genuinely constructive step that can hopefully be taken by many extra fee corporations within the coming years.

What The Consultants Advocate

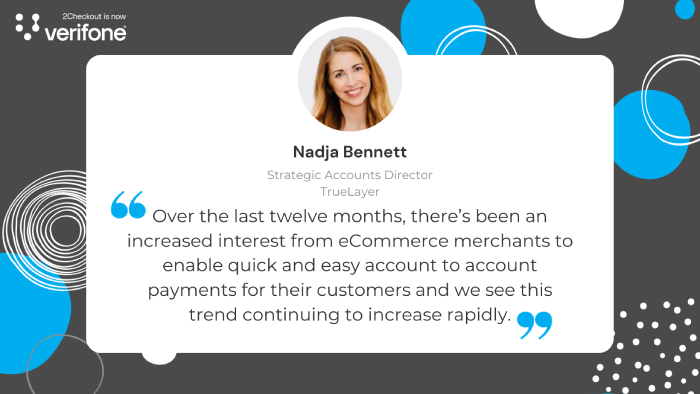

Nadja Bennett, Strategic Accounts Director at TrueLayer:

“Following the introduction of SCA within the UK and Europe, retailers are methods to enhance the checkout expertise with out having to leap by way of hoops of exemptions, to maintain the move as frictionless as attainable all while holding fraud, chargebacks and prices at a minimal. Enter Open Banking! Over the past twelve months, there’s been an elevated curiosity from Ecommerce retailers to allow fast and simple account to account funds for his or her prospects and we see this pattern persevering with to extend quickly in 2023. Study extra in regards to the rise of open banking funds within the UK on this report.”

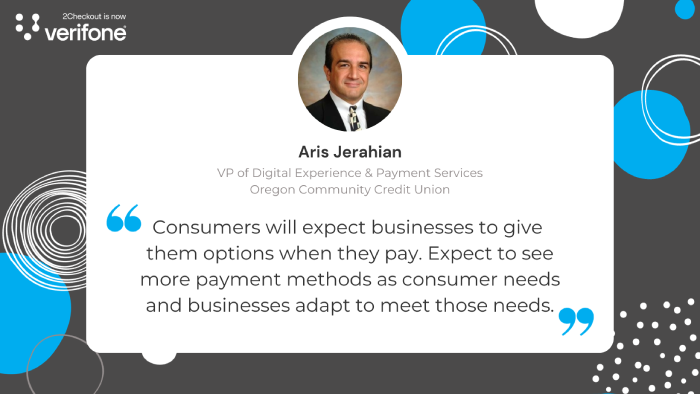

Aris Jerahian, VP of Digital Expertise & Fee Providers at Oregon Neighborhood Credit score Union

“Throughout 2023 eCommerce fee tendencies will revolve round offering a greater, safer procuring expertise. Customers are returning to in-person procuring, however they received’t quit on the comfort of digital funds. Pandemic conduct is right here to remain as customers don’t have any alternative however to make use of digital fee strategies. The checkout course of has develop into crucial a part of a gross sales journey.

Digital pockets choices at the moment are a standard fixture alongside different conventional fee choices and retailers have to get on board. Identical as QR codes – as soon as they appeared to die out, solely to return again with a vengeance. In the present day it’s used as menus, types of fee, tickets, receipts, and many others.

Customers will anticipate companies to offer them choices once they pay. Anticipate to see extra fee strategies as client wants and companies adapt to satisfy these wants.”

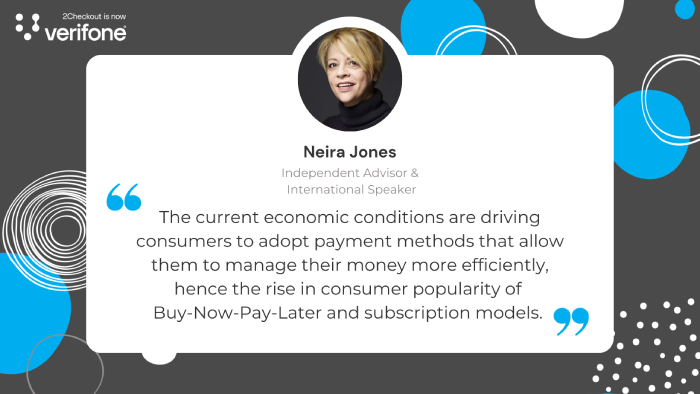

Neira Jones, Unbiased Advisor & Worldwide Speaker, Neira Jones

“Over the previous few years the funds business has develop into more and more digital. The present pandemic has served to speed up that pattern exponentially, with each companies and customers adopting digital funds sooner than they’d in any other case have accomplished. The present financial situations are additionally driving customers to undertake fee strategies that enable them to handle their cash extra effectively, therefore the rise in client reputation of Purchase-Now-Pay-Later and subscription fashions. For companies, Open Banking and real-time funds will enhance in reputation as money move is an rising problem. Consequently, digital B2B funds can solely enhance in adoption, and challenger banks and different new entrants are effectively set to assist.”

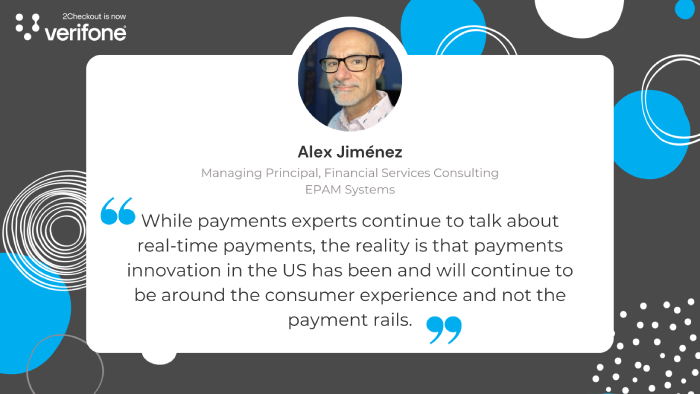

Alex Jiménez, Managing Principal, Monetary Providers Consulting at EPAM Methods

“Whereas funds consultants proceed to speak about real-time funds, the fact is that funds innovation within the US has been and can proceed to be across the client expertise and not the fee rails. COVID has accelerated the adoption of digital funds schemes by forcing extra folks to strive embedded experiences, similar to DoorDash or Postmates, and by shifting to contactless funds together with digital wallets and contactless playing cards. Moreover, P2P adoption can also be rising significantly by small companies who’ve resisted digital funds prior.

The pandemic financial system is driving up increased use of debit playing cards, similar as the strategy behind digital funds, as persons are spending extra on non-discretionary objects and foregoing discretionary objects. Bank card use will stall, whereas Purchase Now, Pay Later (BNPL) schemes acquire extra customers. There’s a renewed curiosity in each day payroll options supplied by fintech corporations, similar to DailyPay. On the similar time, issuers are tightening underwriting requirements for bank cards. The transfer to extra digital funds, additionally means a rise in digital fraud.”

Glenn Geil, EVP – Head of North American Funds Supply, at Endava

“Endava has been a driver of RTP and Open Banking in Europe for a few years. From this deep historical past and having lived by way of how they will come collectively for a robust fee expertise, we imagine that Shopper to Service provider funds through RTP and Open Banking (sometimes called Open Funds) are set to develop into a robust pattern in US funds. The prices of card interchange, as soon as seen as a default price of gross sales, at the moment are a painful margin killer that wants an answer, and Open Funds will be that answer.

We imagine that it’s going to take off first within the eComm area as companies and PSP’s can combine it much like different different fee strategies. On the buyer aspect, the world of wallets and saved fee credentials will restrict the friction of switching to an Open Funds technique.

FedNow’s July launch has introduced the value level of RTP to client utilization ranges, and the current announcement by Early Warning Providers about their frequent financial institution pockets opens the door for future RTP service provider funds to be initiated proper from the banking app, the place many customers go first to test their stability previous to a transaction.

The advantages to the eComm enterprise are completely value the associated fee to combine. The catch is attractive the buyer to modify from the cardboard to a direct financial institution switch. One problem is for these with loyalty playing cards. A enterprise might want to provide you with a substitute worth add, as there have to be some incentive to surrender the factors, however that value-add ought to protect as a lot of the interchange financial savings as attainable.

The larger problem is making the buyer really feel equally able to disputing fraud and errors, as that has develop into the security internet with utilizing playing cards. The difficulty is not going to be the dealing with of precise disputes, however extra the buyer worry of what would occur as soon as they lose their “card-given rights.” Because of this, we imagine that companies catering to the supply of software program, providers, and the subscription supply of products might be the primary to learn, as belief within the supply is considerably increased in these areas. As soon as non-card dispute practices begin to normalize, using RTP and Open Funds will unfold extra quickly to the remaining areas of eComm.”

This RTP/Open Funds pattern will begin to roll out later within the 12 months, however companies ought to begin planning now for the way to telegraph to their consumer base the dispute assurance and loyalty incentives that can entice them to make the change.”

Don Cardinal, Managing Director, Monetary Knowledge Trade

“The Monetary Knowledge Trade (FDX) is unifying the monetary business round a safe, interoperable and royalty-free customary for consumer-permissioned knowledge sharing. Within the funds area, we see tendencies for elevated deal with privateness, safety, and inclusivity – each from customers and regulators. We imagine that world best-in-class authentication schemes like FAPI, which FDX leverages, will proceed to see adoption and use. In the identical manner, we see elevated curiosity and adoption of interoperable requirements in funds as a result of they decrease the obstacles to entry and stage the taking part in subject for small corporations in addition to new entrants into the market led by under-represented teams.”

Conclusion:

As we strategy 2024, the worldwide fee panorama is within the midst of a transformative shift pushed by technological developments, altering client preferences, and the aftermath of world occasions just like the Covid-19 pandemic. This text has delved deep into a number of key tendencies which might be set to form the way forward for funds:

- Contactless Funds & Cellular Wallets

- Embedded Finance & BNPL

- Enhanced Safety & Biometric Authentication

- QR Code Funds

- Actual-Time Funds

- Voice-Activated Funds

- Sustainable & Inexperienced Fee Options

- Good POS Methods

For eCommerce companies, these tendencies underscore the significance of adaptability. The longer term belongs to those that can swiftly incorporate these tendencies and exceed buyer expectations. It’s not nearly providing a service; it’s about enhancing the person expertise, guaranteeing safety, and being socially accountable.

On this ever-evolving panorama, platforms like 2Checkout (now Verifone) play a pivotal function. We offer companies with the instruments and insights wanted to navigate these modifications, guaranteeing they continue to be on the forefront of fee innovation. As we transfer ahead, partnering with 2Checkout (now Verifone) might be essential for your corporation to thrive within the dynamic world of world funds.

{kind=link}