Worldwide enterprise capital in Asia has flourished over the past decade, led by ecosystem platforms (“tremendous apps”), gaming, and e-commerce. Underpinned by a listing of favorable elements like giant populations, a rising center class, and growing technological adoption, the Asia-Pacific area has turn into an extremely wealthy marketplace for tech buyers.

By 2021, whole startup deal worth within the Asia-Pacific exceeded $152 billion—matching the US whole in 2018 and surpassing the growth of the dot-com period. Like a lot of the world, the world skilled a major fundraising decline in 2022, but it surely’s additionally prone to climate the anticipated international downturn in 2023 higher than anyplace else on this planet. China, India, and Southeast Asia, particularly, are swiftly changing into a number of the most tasty enterprise markets on this planet. Nevertheless, to benefit from their funding {dollars} on this culturally and economically various area, VCs should familiarize themselves with its nuances.

As an funding advisor primarily based in Hong Kong, I’ve been actively concerned within the personal funding markets within the Asia-Pacific for the final decade. One factor I’d emphasize to buyers concentrating on Chinese language, Indian, and Southeast Asian markets is that though they’re geographically related and all thought of “rising markets,” the enterprise alternatives in every are distinctly completely different. That stated, as regulatory environments change and M&A-happy tech giants present growing competitors to VC, what occurs in a single nation can have a major impact on markets in others. Listed here are the tendencies that I see shaping the enterprise atmosphere of those markets within the coming years.

China: Tech Giants Are Supplanting VC

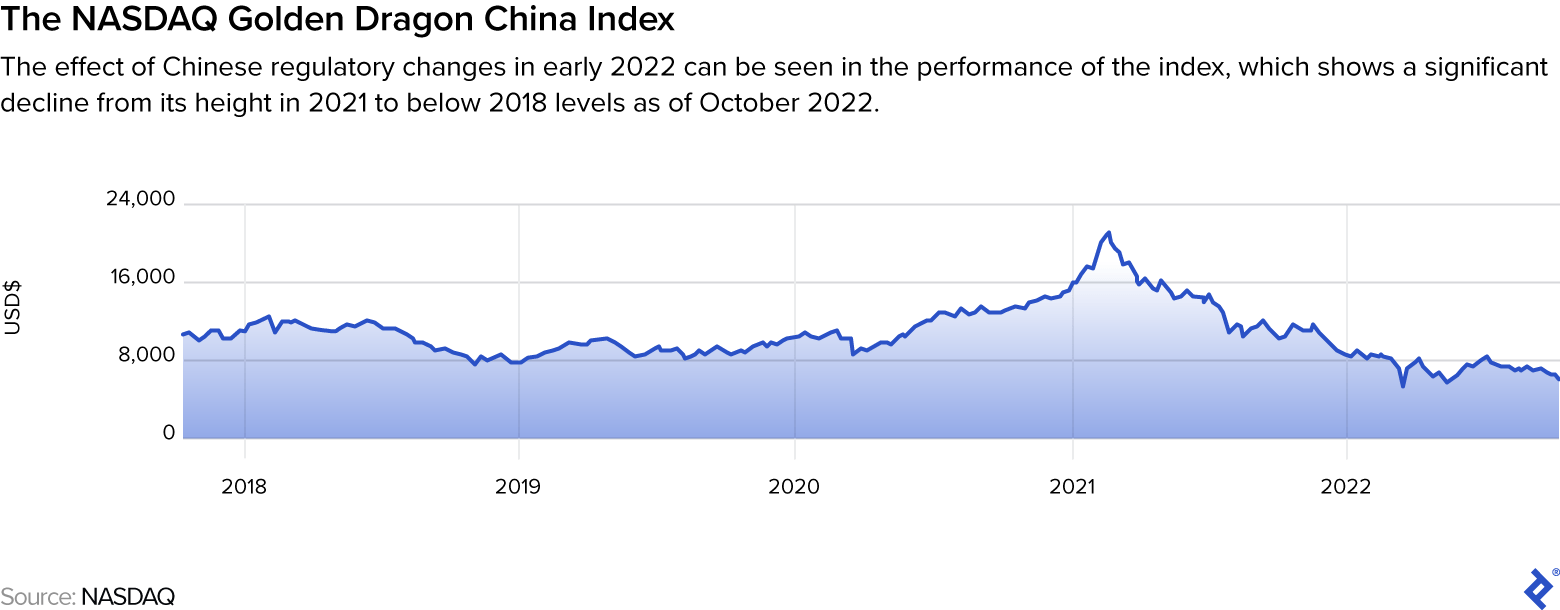

To know the state of enterprise capital in Asia, you need to first perceive what’s occurring in China, which has lengthy been one of the crucial in style markets on this planet for overseas VC buyers. The late Nineteen Nineties and early 2000s have been a time of unimaginable alternative for these buyers as Western-educated Chinese language entrepreneurs lined up a capital pipeline to spice up innovation within the expertise sector, finally constructing a number of the nation’s most formidable tech giants.

The early success tales of Japan-based SoftBank investing in Alibaba and South Africa-based Naspers investing in Tencent have since attracted extra overseas VC buyers on the lookout for the subsequent large guess, and the market continues to thrive in its maturity.

As early, overseas VC-backed tech firms step by step grew into the giants we all know as we speak, in addition they modified the aggressive panorama of many industries in China—together with the VC market itself.

China-based tech giants are actually targeted on constructing tremendous apps. And quite than growing new merchandise in-house, they’re as a substitute leveraging their hefty wallets and utilizing mergers and acquisitions to develop. This opportunistic funding technique is now disrupting the enterprise funding market within the nation that VC companies as soon as dominated.

International Traders Face New Obstacles

For his or her half, many smaller and early-stage tech firms in China have come to favor the monetary backing of home tech companions to funds from overseas VC companies. This sort of partnership is successfully a trusted model’s stamp of approval for the corporate’s enterprise mannequin and thus attracts person visitors. The inclusion of the goal agency’s product choices within the buying agency’s broader app ecosystem additionally sweetens the place, as partnership alternatives improve from the extra visibility.

International buyers have additionally begun to face competitors from state-backed VC funds. The Chinese language authorities’s regulatory efforts to reduce the affect of home tech giants have prompted founders of recent tech companies to look to those state-supported funds to assist win the federal government’s favor and cut back burdensome oversight.

Though the Chinese language authorities and regulators may calm down the crackdown every now and then to spice up the nation’s financial progress, I don’t foresee a directional change by way of its coverage and initiatives towards the broader tech sector. The emphasis on taming the affect of tech giants and supporting the event of sure strategic tech sectors—together with semiconductors, synthetic intelligence, and electrical autos—will not be prone to be a short-term posture.

To Break By means of, Supply Strategic Worth

For overseas VC buyers who’re undaunted by these new limitations to entry and nonetheless desirous to faucet into the expansion potential of China’s tech market, it’s important to know that patrons should carry extra to the desk than simply cash. Strategic positioning is vital.

Does the investing agency have particular trade experience or a spotlight that would give the goal firm entry to new markets? If the goal firm plans to succeed in abroad, can the investing agency speed up enlargement?

Whereas I used to be on the principal investments crew of the worldwide reinsurer Swiss Re, I led a cornerstone funding in a Chinese language on-line healthcare firm. In response to latest estimates, the digital healthcare market in China is projected to succeed in $46 billion in 2022 and proceed to develop at a compounded annual fee of 12.98%, which might imply a $84.7 billion market by 2027. In 2018, nonetheless, the sector was nonetheless in its infancy, price solely $15.2 billion. It was one of many hottest spots for progress, and competitors amongst institutional buyers was fierce.

As a overseas investor coming into the combo, we have been competing towards Chinese language and worldwide sovereign wealth funds, Chinese language state-backed funding companies, and quite a lot of blue-chip buyers for an allocation. Ultimately, we tipped the deal our approach by leaning into our experience within the insurance coverage trade. Our agency had a protracted historical past of investing in insurance coverage and insurtech firms everywhere in the world and will advise the goal firm on methods to monetize its healthcare platform by partnerships with insurers.

Different offers weren’t as turnkey, so we fashioned a consortium or partnership to co-invest with a extra strategic tech large. In these instances, our agency needed to show how we may strategically place ourselves as a high-value accomplice that would profit the China-based tech large and mix forces to win the allocation.

For instance, we wished to put money into a Chinese language startup that was additionally being courted by a Chinese language tech large. We have been capable of persuade the tech large to allow us to co-invest within the startup with it by providing to help the tech large’s abroad acquisitions in alternate.

India: A New Vacation spot for International VC

Not surprisingly, many overseas VC buyers have been delay by the more and more restrictive atmosphere in China. A great variety of them are actually selecting an alternate market with related progress prospects by actively redirecting their capital to India’s tech sector.

Among the many greatest winners of this exodus are consumer-focused startups, which reached a complete worth of $1.6 billion in 2022. These companies are prone to desire a market that’s much less scrutinized than China, the place any app with affect on shopper conduct is carefully watched. Because of this, the buyer app growth market in India is anticipated to develop at a compounded fee of 9.2% yearly for a minimum of the subsequent 4 years, in response to latest projections.

Additional bolstering this anticipated progress in app growth is the truth that India is about to overhaul China because the world’s most populous nation in 2023.

Overvaluation Is an Ongoing Concern

What buyers want to concentrate to are the sky-high valuations ensuing from an excessive amount of cash chasing too few offers. India’s public fairness market has all the time traded at a premium in comparison with China’s, and that is still true as we speak. Though a wealthy public fairness market valuation doesn’t essentially indicate a wealthy personal market valuation, it usually acts as a comparability benchmark. With much more funding pouring into India’s tech scene, overvaluation will proceed to be a problem in coming years—although latest rate of interest boosts could assist include it.

Regardless of these considerations, there are nonetheless loads of good causes to put money into India’s tech sector. Many Indian tech firms, particularly fintech firms like Pine Labs, Ayannah International, Razorpay, and others, need to develop into Southeast Asia—one thing many Chinese language tech giants started to do in 2015.

Whether or not Indian tech firms can efficiently faucet into the Southeast Asian market is one thing to look at within the subsequent few years. In the event that they succeed, they could be capable to justify the wealthy valuations we see as we speak. In any other case, the Indian market may more and more really feel like one other bubble ready to burst.

Traders, Know Your Limits

As when coping with Chinese language companies, buyers ought to articulate to Indian goal firms the strategic worth they will provide and leverage that because the grounds for worth negotiation. This technique could also be not possible in the event you’re bidding towards a big institutional investor. In that case you ought to be ready to stroll away if the valuation turns into unjustifiable.

That type of calculation can really feel painful within the quick run, however keep targeted on the lengthy sport. Whereas at Swiss Re, I checked out a possible funding alternative in an Indian insurtech firm. Sadly, the goal firm had put us in a bidding competitors with SoftBank. We calculated that matching SoftBank’s provide would wipe out our projected returns, so we referred to as it off.

SoftBank could also be paying the value for its magnanimous method, nonetheless, because it now faces multibillion-dollar losses linked to its aggressive funding technique. The ethical? While you’re contemplating investing in India, self-discipline is essential.

Southeast Asia: Interesting Alternatives for Secondary Traders

Southeast Asia, the third high-growth market within the area, appears to be the right vacation spot for overseas buyers unwilling to navigate China’s growing insularity or India’s overheated markets.

A veritable VC desert simply 15 years in the past, Southeast Asia is now one of the crucial promising areas to put money into, with firms comparable to Sea Restricted, Seize, GoTo Group, and others driving the tremendous app wave to new heights. After the profitable itemizing of some tech firms from Southeast Asia in 2020, the pattern has steadily grown, and buyers are lastly prepared to purchase into the world’s alternatives.

Nevertheless, valuations in a lot of the area’s nations have fallen effectively beneath their itemizing costs, which ought to make buyers cautious. These sluggish share worth performances is likely to be attributable to macroeconomic elements—like geopolitical dangers, and rate of interest hikes within the US and the EU—that don’t have anything to do with the corporate’s fundamentals. Whatever the trigger, an IPO may not be a horny exit path for a lot of VC buyers within the close to time period.

Liquidity Occasions Are on the Horizon

Though IPO prospects could also be poor, the subsequent few years will see a wave of secondary funding alternatives. The earliest cohort of VC companies concentrating on Southeast Asia raised their funding from restricted companions (LPs) between 2010 and 2015. VC funds often have a fund lifetime of seven to 10 years with the choice to increase by just a few extra years upon expiration. Then, they must return the capital to their LPs.

Because of this, most of those funds might want to pursue liquidity occasions someday between 2025 and 2027. If the IPO market continues to lag on this area, early-round VC funds and buyers can be open to negotiating a secondary sale to non-public buyers.

Enticing Secondary Funding Alternatives Are on the Rise

In rising markets, secondary alternatives are interesting as a result of investing in additional mature startups can provide higher risk-adjusted returns. As a secondary investor on this market, you might also discover motivated sellers who can be prepared to barter a reduction on their firm’s newest valuation as a result of they’re searching for a fast payout and exit.

Proper earlier than embarking on my freelancing profession, I labored with the abroad investments crew of Tencent, one of many Chinese language tech giants that aggressively invested within the area. I used to be chargeable for managing the group’s investments in Southeast Asia, so buyers trying to exit approached me usually. Lots of them have been prepared to supply a 20% to 50% low cost on the goal firm’s newest valuation. For unrelated causes, we wound up not investing, and looking back, our selection was most likely the precise name. Given the continued correction within the share costs of the area’s tech firms since their itemizing, these discounted valuations probably would have nonetheless been too excessive.

To Compete With Tech Giants, Supply Autonomy

Tencent, China’s Alibaba, and India tech giants like Razorpay, Moglix, and Pinelabs are extra often competing with international VC buyers for a foothold in Southeast Asia. Given their technique to develop by acquisition, these bigger cash-rich firms are sometimes extra prepared to assign a heftier price ticket to a goal firm than a overseas VC investor is likely to be prepared to pay. And current shareholders could favor to promote the corporate to those strategic buyers quite than to overseas enterprise buyers focusing totally on monetary returns.

Whereas there are a lot of causes a small firm may need to be acquired by a tech large, there are additionally causes it would favor to go one other route. Acquisition provides startups little selection however to align their technique with their acquirer. Enterprise capital, however, can provide an organization extra autonomy. To keep away from bidding wars with tech giants, international buyers on the lookout for early-stage alternatives within the space could be well-advised to focus on companies that need extra management over their progress than the tech giants can provide.

Interconnected Alternatives

With the Asia-Pacific promising to be a relative vibrant spot throughout a doubtlessly gloomy 2023, VC buyers planning to turn into extra energetic within the area want to know the forces driving the state of enterprise capital in Asia within the subsequent three to 5 years. It’s crucial to concentrate on the native elements in every market and submarket, and the way every market impacts the influx and outflow of capital by the others.

In the end, these complexities provide not solely challenges, but additionally significant alternatives to overseas VC. The number of market forces and levels of company maturity throughout China, India, and Southeast Asia give buyers the prospect to hedge towards volatility in some areas by balancing their portfolios in others. Doing so correctly will empower buyers to seize the mixed general progress of all three.

{kind=link}